Why you Should Never Delay the Payment of your Credit Card Bills

When used smartly, with prudence and financial discipline, credit cards can be quite a convenient financial tool that can help you manage your rolling money better. However, anyone who has ever missed a credit card payment knows that missing timely payments of your credit card bill is one of the cardinal financial sins. Missing the due date of your credit card bills can have significant financial implications that could affect your overall credit worthiness.

When used smartly, with prudence and financial discipline, credit cards can be quite a convenient financial tool that can help you manage your rolling money better. However, anyone who has ever missed a credit card payment knows that missing timely payments of your credit card bill is one of the cardinal financial sins. Missing the due date of your credit card bills can have significant financial implications that could affect your overall credit worthiness.

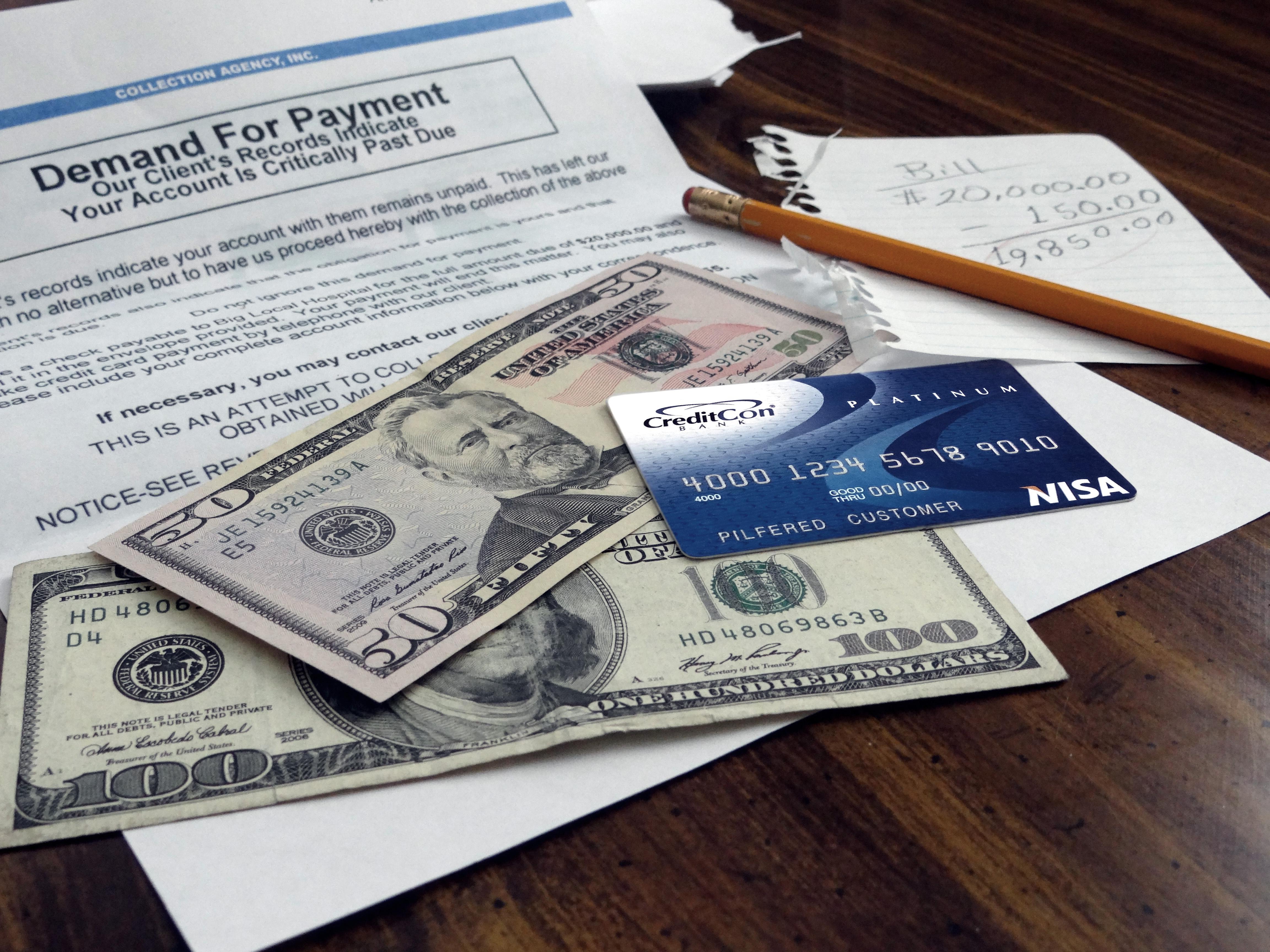

Many falsely believe that paying the minimum amount due on your credit card bill is sufficient to avoid interest on the outstanding bill amount. However, your entire outstanding credit card bill will attract interest charges, irrespective of the amount that you have paid. Missing a credit card bill payment means a late fee will be levied when you fail to pay the minimum amount due by the bill due date. The longer the delay, the charges and late fees keep piling on and a heavy interest is levied on outstanding bill amount.

Depending on your card issuer, the annualized interest rate on this outstanding amount can go up to as high as 45% p.a.While there is a short window of interest free grace period that the RBI directs card issuers to allow and you can avail this window to pay any pending bills that you may have. However, missing a payment means that your credit score is likely to be adversely affected and the card issuer may reduce your credit limit too.

If, for whatever reasons you are unable to pay your outstanding credit card bill, contact your credit card issuer to convert your purchases into equated monthly installments. However, it may cause problems should you decide to apply for a consumer loan in the future.

Tags: budgeting, credit, credit card debt, debts, financial planning, money